All Categories

Featured

Table of Contents

One more opportunity is if the deceased had an existing life insurance policy policy. In such instances, the designated beneficiary may get the life insurance policy proceeds and use all or a portion of it to repay the home loan, allowing them to stay in the home. best home buyers protection insurance. For people that have a reverse mortgage, which permits individuals aged 55 and above to acquire a mortgage based on their home equity, the financing interest builds up gradually

Throughout the residency in the home, no repayments are called for. It is essential for individuals to very carefully intend and take into consideration these elements when it concerns home mortgages in Canada and their influence on the estate and heirs. Looking for assistance from legal and economic professionals can help guarantee a smooth transition and correct handling of the mortgage after the home owner's passing away.

It is vital to recognize the readily available choices to make certain the mortgage is appropriately handled. After the death of a property owner, there are numerous choices for home loan settlement that depend on different variables, consisting of the regards to the home mortgage, the deceased's estate planning, and the dreams of the successors. Here are some usual options:: If multiple beneficiaries desire to assume the mortgage, they can come to be co-borrowers and continue making the mortgage repayments.

This choice can supply a clean resolution to the mortgage and disperse the remaining funds amongst the heirs.: If the deceased had a present life insurance policy policy, the designated beneficiary may receive the life insurance policy earnings and use them to settle the mortgage (house insurance for home loan). This can enable the beneficiary to remain in the home without the worry of the home loan

If no person remains to make home mortgage repayments after the homeowner's fatality, the home loan financial institution has the right to foreclose on the home. The effect of repossession can differ depending on the situation. If an heir is named yet does not market the house or make the home mortgage settlements, the home mortgage servicer could launch a transfer of ownership, and the repossession can drastically harm the non-paying successor's credit.In instances where a property owner passes away without a will or trust, the courts will certainly assign an administrator of the estate, generally a close living relative, to disperse the assets and liabilities.

Insurance And Mortgage Services

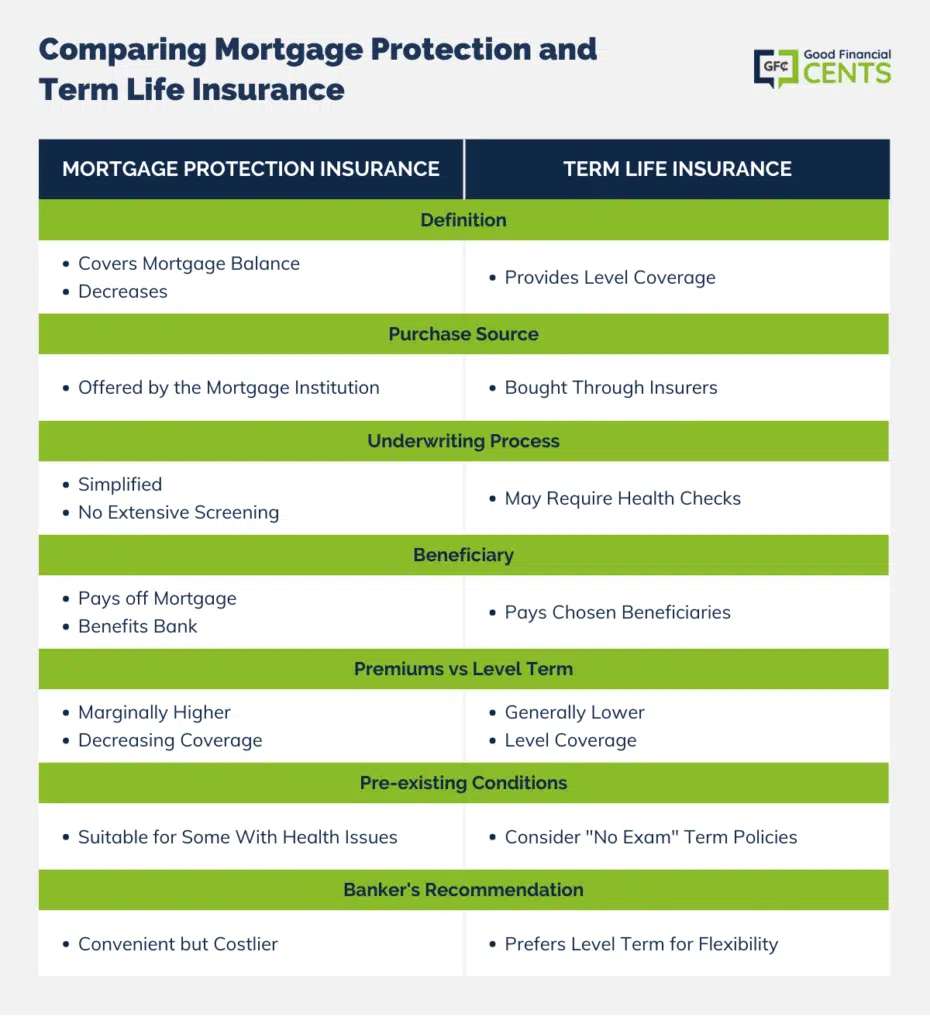

Home loan security insurance coverage (MPI) is a kind of life insurance coverage that is especially developed for people who want to make sure their home mortgage is paid if they pass away or come to be impaired. Occasionally this type of policy is called home mortgage settlement security insurance.

When a bank possesses the large majority of your home, they are liable if something occurs to you and you can no much longer pay. PMI covers their risk in case of a repossession on your home (td mortgage credit protection). On the other hand, MPI covers your risk in the occasion you can no more pay on your home

MPI is the kind of home loan protection insurance every homeowner must have in place for their family members. The amount of MPI you require will differ depending upon your distinct circumstance. Some variables you should take into consideration when thinking about MPI are: Your age Your health and wellness Your monetary circumstance and resources Other types of insurance policy that you have Some people might think that if they currently possess $200,000 on their home mortgage that they need to get a $200,000 MPI plan.

Term Insurance Mortgage

The concerns individuals have concerning whether or not MPI is worth it or not are the same questions they have regarding getting various other kinds of insurance policy in general. For many people, a home is our solitary biggest financial obligation.

The combination of anxiety, sadness and transforming household dynamics can cause also the most effective intentioned people to make expensive errors. mortgage insurance with critical illness cover. MPI addresses that issue. The worth of the MPI plan is directly tied to the equilibrium of your mortgage, and insurance policy earnings are paid directly to the bank to take care of the remaining equilibrium

And the biggest and most demanding financial issue dealing with the surviving member of the family is resolved instantly. If you have health problems that have or will produce troubles for you being approved for routine life insurance, such as term or entire life, MPI might be a superb choice for you. Typically, home mortgage protection insurance plan do not need medical examinations.

Historically, the quantity of insurance coverage on MPI policies dropped as the balance on a home mortgage was decreased. Today, the protection on a lot of MPI plans will stay at the same degree you purchased at first. If your original mortgage was $150,000 and you acquired $150,000 of home mortgage protection life insurance, your beneficiaries will currently obtain $150,000 no matter just how much you owe on your home mortgage.

If you intend to repay your mortgage early, some insurer will permit you to transform your MPI policy to one more sort of life insurance coverage. This is among the questions you might desire to deal with in advance if you are considering paying off your home early. Costs for home loan protection insurance coverage will differ based upon a variety of points.

Property Insurance With Home Loan

Another element that will certainly influence the costs quantity is if you get an MPI plan that offers coverage for both you and your spouse, offering benefits when either one of you dies or becomes impaired. Understand that some firms may require your policy to be reissued if you re-finance your home, but that's normally just the situation if you bought a plan that pays only the equilibrium left on your home mortgage.

What it covers is really narrow and plainly specified, depending on the alternatives you choose for your specific plan. If you die, your home loan is paid off.

For home loan defense insurance, these kinds of extra protection are added on to policies and are known as living benefit cyclists. They permit policy holders to tap into their mortgage defense advantages without passing away.

For situations of, this is usually currently a free living advantage offered by most business, yet each firm specifies advantage payouts differently. This covers health problems such as cancer cells, kidney failure, cardiac arrest, strokes, mental retardation and others. ace disaster mortgage protection insurance. Business typically pay in a swelling sum depending on the insured's age and extent of the health problem

Unlike the majority of life insurance coverage policies, getting MPI does not need a clinical examination a lot of the time. This indicates if you can not obtain term life insurance coverage due to an ailment, an ensured concern mortgage security insurance coverage policy might be your finest wager.

No matter of who you choose to discover a policy with, you must always go shopping about, due to the fact that you do have choices. If you do not qualify for term life insurance coverage, after that unintended fatality insurance may make more sense because it's warranty problem and suggests you will certainly not be subject to medical examinations or underwriting.

National Mortgage Protection

Make certain it covers all expenditures connected to your home loan, consisting of interest and payments. Consider these elements when choosing exactly just how much insurance coverage you believe you will require. Ask exactly how quickly the plan will certainly be paid out if and when the primary earnings earner dies. Your family members will be under sufficient psychological anxiety without needing to question for how long it might be before you see a payment.

{kind=link}

Latest Posts

Final Expense Insurance Plan

Burial Expense Insurance Companies

Funeral Cover For Over 60